2025 Market Share Segmentation: A Comparison of LCD and OLED Dominance

2025/10/13

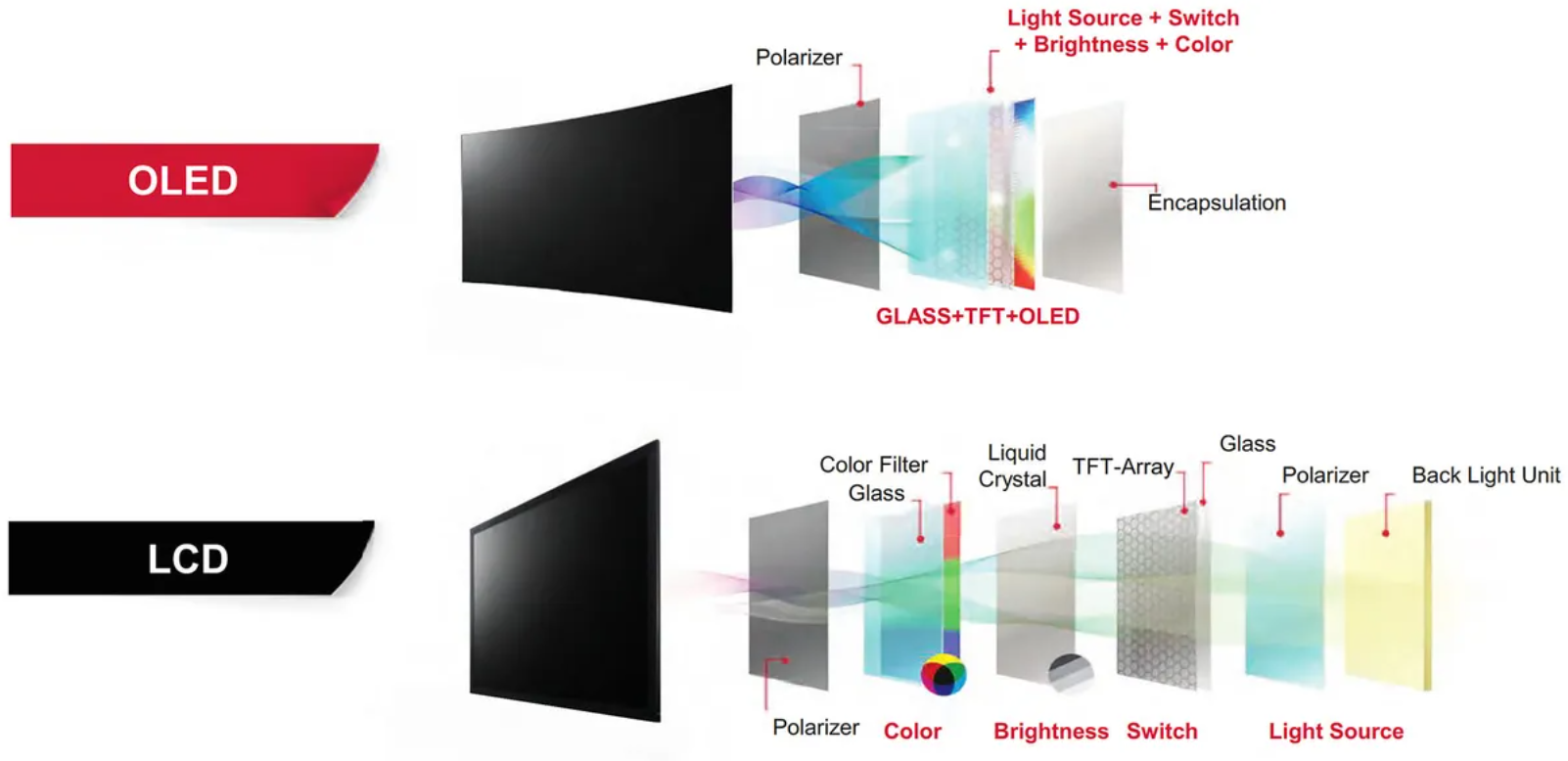

2025 Market Outlook

l Large size panels (≥9inches) are projected to grow 2.8% YoY to about 910 million units.

l LCD shipments reach 873.9 million units (+2.2% YoY) while OLED shipments rise 19.0% YoY.

Product?level trends

|

Segment |

2025 YoY change |

Driver |

|

LCD TV |

–3.4% |

TV demand softening |

|

LCD Monitor |

–1.8% |

Traditional PC slowdown |

|

LCD Tablet |

+17.5% |

Mobile office & education |

|

LCD Notebook |

+4.2% |

High performance thin and light laptops |

|

OLED TV |

+3.1% |

Modest growth |

|

OLED Monitor |

+60.9% |

IT monitor boom |

|

OLED Notebook |

+45.9% |

Premium notebooks adopt OLED |

|

OLED Tablet |

–2.3% |

Slight decline |

Takeaway: Strong demand for mobile PC screens (tablets & notebooks) offsets the decline in TV and traditional monitor shipments, keeping overall large size panel shipments positive.

Regional & Vendor Share

l LCD: Mainland China 67.6%, Taiwan 21.0%, South Korea 8.1%.

l Top LCD vendors: BOE 37.1%, ChinaStar 16.8%, Innolux 11.4%.

l OLED: South Korea 83.7%, Mainland China 16.3%.

l Top OLED vendors: Samsung Display 54.3%, LG Display 29.4%, EDO 13.9%.

l Revenue: Total 2025 large size panel revenue ≈ US$72.7bn, with 83.7% from Mainland China, 18.0% from South Korea, 14.7% from Taiwan.

l Revenue leaders: BOE 29.7%, ChinaStar 20.2?%, LGDisplay 12.4%.

Strategic Highlights

l LCD: Chinese manufacturers expand 8.6?generation IPS factories to capture IT display share; LGDisplay, Sharp focus on cost structure improvements.

l OLED: Korean players shift to IT applications (monitors, notebooks) to compensate for weak TV OLED; they also leverage high end tablet customers (Apple, Samsung) – tablet OLED shipments still +3.6% for those clients.

All data are sourced from Omdia’s latest “Large?size Display Panel Market Tracker” (published 13 Oct 2025).